Bankocracy #2 — A review

by Sue Peters, GPNY

INTRO

This is a review of the second episode of John Titus' series, The War for Bankocracy: Unmasking the Hidden Power of Central Banks.

The word 'bankocracy' means rule by banks. The goal of the series is to inform people of the current attempt by the Federal Reserve to convince Congress and the American public that the Fed Reserve should have total sovereignty over money creation — that is, have no oversight by our Congress. But, remember, the Federal Reserve was created by Congress in 1913 by the Federal Reserve Law, and Congress can take back its constitutional power to create money from the Fed by passing new laws.

On the other hand, the European Central Bank [ECB] is the sovereign of money creation in Europe. There is no oversight by any government. The ECB was created by international treaty between European central banks, now numbering 20 signers. To change the ECB would require all 20 central banks to agree. There is no oversight from any of the European countries or central banks over the ECB.

PRIVATE AND ANONYMOUS CONTROL OVER THE CREATION OF MONEY

The parts of the Federal Reserve which have the "money power" are privately-owned:

- 12 regional Federal Reserve Banks ('FED Banks') (owned by member commercial banks)

- thousands of commercial banks (owned by shareholders)

When one tries to research the owners of the largest commercial banks, one finds that ownership is legally hidden. The identity of major shareholders is kept anonymous. We do not know who is running the FED! The public needs to know who controls this sovereign power wielded over every citizen!

WHAT ARE THE POWERS OF THE PRIVATE FEDERAL RESERVE?

- The 'money power' consists of CREATING what we all use for money:

-

[A] CASH: The Federal Reserve Board ISSUES every cash dollar. The member banks buy the cash from the Fed. The cash circulates when bank depositors ask for cash.

-

[B] CHECKING ACCOUNT BALANCES: There are two important steps:

-

-

I. Commercial banks CREATE electronic deposits in our checking accounts. !!! WHAT !!! Yes — here is how. When banks make loans, they CREATE the loan principal as a deposit in the borrower's account, all with interest to the bank! In addition, when banks buy bonds, they CREATE the payment as a deposit in the seller's account! !!! PRESTO !!!

-

II. To create these deposits, the bank needs reserves, only created by the Fed Banks. The borrowed loan principal will most probably be transferred by check to a receiving party at another bank. The transaction will not be finalized at the receiving bank, until reserves, equal to 100% of the check amount, are moved from the borrowers' FED Bank to the receiver's FED Bank. Thus, reserves are absolutely necessary for bank-created deposits to work as our money supply. And the power to create reserves is found only in the FED Banks.

-

Additionally, the Federal Reserve controls bank deposit creation in the following ways:

-

-

set important interest rates.

-

controls the 'reserve requirement' for banks. Legally, bank deposits are not money but a promise-to-pay money on demand (when the customer withdraws cash or writes a check). So the bank is required to hold cash deposits at its Fed Bank, known as 'reserves'.

-

Federal Reserve Banks CREATE all reserves needed by the banks. Here are two ways the FED Banks do this:

-

-

The FED buys a bond from a bank, and pays by creating reserve deposits for the bank.

-

The FED buys a bond from a private party, and pays by creating reserve deposits for the seller bank. Simultaneously, the seller bank creates a deposit in the seller's checking account. This procedure was begun during the 2020+ pandemic and caused a huge inflation we are still living with.

ORIGIN OF CENTRAL BANKING

The model of a privately-owned central bank, with anonymous ownership, creating money, began with the English Parliament giving a legal charter to the Bank of England in 1694. There was no government ownership, and the identify of the controlling share owners was kept hidden by legal devices. It was given the sovereign right to create paper money for the nation, accepted by the national government. It loaned out the paper money for interest. It also made loans by creating deposits in an account ledger. Just like today.

Over time, the Bank of England grew more and more powerful. It funded England's wars. It concentrated wealth in the elites. It caused the growth of huge national debts. It indebted working people. Today, a successor of the Bank of England, the Federal Reserve System, does the same.

Remember: all war depends on money. Remember: the Federal Reserve System decides who to loan to and for how much. Look around. Huge loans are going to weapons manufacturers, pharmaceutical companies, multinational corporations. This private system has been shaping our society for decades.

Credited to Thomas Jefferson: " … banking institutions are more dangerous to our liberties than standing armies…"

2025: Austerity Coupled With Greed of 1%

by Eugene Woloszyn GPCT

Trump's Secretary of Commerce Howard Lutnick bluntly stated: You have almost $4 Trillion of entitlements (Social Security, Medicare & Medicaid) and MUSK will cut $1 Trillion

(over 25%). You know Social Security is wrong, you know Medicare is wrong, so MUSK is going to cut $1 Trillion. Our objective is to balance the budget.

Independent Newspaper of Britain, 2-20-25.

Commerce Secretary Howard Lutnick (backed by MUSK) & Treasury Secretary Scott Bessent are the HEAVY WEIGHTS in the Trump Cabinet. They both battled for the top spot at Treasury. Both are decades long Wall Streeters & hedge fund manipulators. They & Trump want these massive budget cuts in order to provide big tax decreases to corporations & the top 10% of the population. They want to repeal (but also expand) the tax cuts for elites enacted by Reagan in 1980s, in 2001(Bush II), in 2017(Trump I) & in 2025 Trump II). However, the math is crazy. The US budget deficit in 2024 was $2 Trillion. Congressional Budget Office estimates federal debt will increase by $20 Trillion in the next 10 years (absolutely shocking). In order to continue the expiring tax cuts from Trump's 2017 tax package, it will cost $4.5 Trillion over 10 years. What a mess created by both parties.

The only "success" of Trump's first term was his 12-2017 tax bill. What did it accomplish?

TRUMP CUT BUSINESS TAXES 40% in 2017. These were made PERMANENT, unlike other cuts which must be renewed in 2025. Trump this year quietly proposes 27% further business tax cuts. This is not an exaggeration; business tax rates fell from 35% to 21% in 2017. Although not given much publicity, Trump proposes a further cut to 15% in 2025. What if you could get a PERMANENT 40% cut in your mortgage or vehicle payment or your credit card interest rate? Working people got a 3%-5% cut in taxes in 2017, & business got a 40% cut. How did Democrat leaders not scream from the rooftops? Because the fix was in.

In a similar situation to today, when Trump won by narrow vote in 2016 & 2024, what did the Democrats do? Let's go over this sad history. Did Democrats say that a 40% business tax cut was a rip-off & a betrayal of working people? NO. Did Democrats demand that the 40% business tax cut be reduced to 20% or 10%? NO. Did they mobilize their campaign organization from the previous year & its vast email list? NO. Like Obama in 2009 & 2010, Democrats were weak & did not defend the working class. Obama paid the price with a massive Republican election victory in 2010, which ended Democrat control of Congress. Democrat leaders knew that their corporate & elite funders wanted this 2017 tax bill to pass—so they made phony arguments on small issues. It could have been different because tax bill passed by only a couple votes in the Senate. DEMOCRATS BETRAYED WORKING PEOPLE & paid the price again in 2024 election.

Did Democrat leaders try to block the bad changes that weakened the alternative minimum tax that Trump & his cronies hated? NO. When the rich get big tax breaks, working people are squeezed immediately or down the road. And the down the road is happening in 2025. Austerity is happening with federal workers & cutting items for small farmers that were included in Biden's Inflation Reduction Law. Watch some of the Tik Tok videos of sorry Trump voters losing their jobs or small farmer federal assistance. It is painful.

Did Democrat leaders try to block the sweetheart deal that allowed $2 Trillion in corporate profits stored in Europe & elsewhere waiting 10 years for the moment when these super profits could be repatriated at the shocking low rate of 11% tax? No. Democrats, including Bernie Sanders, did not publicize & fight at the grass roots on all of these populist Issues of "US AGAINST THEM". Instead, Democrat leaders in 2025 are pushing the same elite demand for removing the cap on state & local tax deductions on income tax forms. There is now a $10,000 Cap on these deductions & removing the cap would primarily benefit higher income people in Democrat ruled cities in the north & west.

Democrats are supposedly trying to win back the support of working people. How many of them have state & local tax deductions over $10,000. Why don't Democrats use their campaign structure, email networks, & local demonstrations to clamor for a stop to Trump's quiet plan to further decrease business taxes in 2025 by a shocking 27%?

The demand should be NO BUSINESS TAX CUTS this year.

The 40% cut last time was outrageous. If Democrat leaders had guts, they would also demand that business taxes be raised this year by 20% to reverse the greedy corruption of the 2017 tax bill. In 2017, Democrat leaders rolled over & let working people get screwed. TRUMP was not able to get his tax bill passed until December of his first year. There is still time to organize against it. There are so many proclamations & events happening daily, it's easy to get distracted from the big economic & financial power plays & maneuvers underway. When the crash occurs, the 2025 austerity cuts to safety net programs will be deeply & painfully missed.

THIS COUNTRY SHOULD NOT BE RIGGED BY PEOPLE WHO ALREADY HAVE EVERYTHING.

TRUMP: CAP CREDIT CARD INTEREST RATES AT 10%

by Eugene Woloszyn GPCT

During the last campaign Donald Trump stated: We can't let banks make 25% & 30%

interest rates on credit cards. He called for a temporary 10% cap to lower living costs. The average US credit card balance is $6,500, costing $116 per month in interest alone plus a payment to reduce the principle. The average credit card rate is 22% on unpaid balances. If the interest rate was reduced to 10%, interest payment per month would be cut in half to $54. (CNN, 9-24-24).

CREDIT CARD COMPANY PROFITS ARE OVER 50%.

This was admitted by CEOs of MasterCard & Visa at Senate Hearing chaired by Republican Josh Hawley of Arkansas & went VIRAL in a short Tik Tok video. Grocery profit margins are about 3%. Profit margins over 10% are unusual. 50% profit margins are highway robbery & for centuries were called USURY & condemned by all religions as blasphemous & unjust. But now the churches are silent.

CREDIT CARD COMPANIES ARE ALL OWNED BY BIG BANKS.

The source of the interest rate rip-off is Wall Street. And credit card companies also hurt business owners with swipe fees that are very complicated, changing & onerous. The average card rate is now 22%, which is 6% higher than before Covid mass unemployment. This is a clear example of extreme corporate profit gouging in a time of catastrophe. It leads to harsh inflation, family stress & greater inequality.

AMAZON & HOME DEPOT CARDS

charge 30%. New credit cards in fine print have interest rates of 36%. These rates make it almost impossible to get out of debt, especially for families. But credit unions have a cap of 18.5% but still make money. There is a cap for US soldiers, but it is 36%. Outrageous how bank lobbyists & their bought off politicians treat soldiers, while hypocritically thanking them profusely for their service.

Up to the 1960s, many states had populist, grass roots pressure that forced legislatures to pass maximum interest rates, usually about 6%. Arkansas had a 10% maximum rate written into its 1874 Constitution. Banks & media convinced the public to pass a new Constitutional Amendment in 2011 raising the cap to 17%. But now Arkansas card holders pay over 22% because the US Supreme Court in 1978 ruled that the interest rate of location of credit card company home office (N. Dakota) determines interest rates across the US. Bank lobbyists buy off corrupt state legislators & governors.

DEEPER THAN INTEREST RATE CORRUPTION IS THE LITTLE-KNOWN TRUTH OF HOW BANKS MAKE THEIR MONEY.

97% of all US dollars are electronic. Banks make loans by depositing digits in the borrower's accounts & then borrowers repay these loans over years or decades PLUS INTEREST. Homes cost 2X or 3X the selling price or are not attainable for many seeking them. The same hidden system occurs with credit cards. Banks create money that is paid to the vendor when you buy shoes with a credit card. The credit card issuer is a consortium of big banks who charge you over 22% interest & the banks make over a 50% profit on this crooked credit card racket. But instead of banks creating money out of thin air, why don't bank loan out depositor money held at their banks? BANK RUNS are the greatest nightmares of bankers. The most painful examples were 1929, during the Savings & Loan collapse in the late 1980s & 2008. This is not an impossible relic of the past. In 3-2023, high tech darling Silicon Valley Bank lost $50 billion in deposits in a run in 24 hours before government closure. Two others $100+ billion banks collapsed at the same time.

Commercial banks are the only US corporations that can legally create money in depositor accounts when making loans. The borrowers must repay loans plus interest or lose their collateral. How much new money is created by this bank money creation? According to statistics of the Federal Reserve Bank of St. Louis, it is $2.7 Trillion per year. When the US federal discretionary budget is only $1.6 Trillion per year, it's clear that commercial banks decide the investment direction of the country.

Which insiders get loans at what interest rate? Loans to speculators, hedge funds, loans to send more jobs overseas & further deindustrializing the US, fossil fuels, armament companies, but little sustainable lower priced housing. This must change.

For a deeper discussion of these issues, see GreeningTheDollar.org.

The Abuse of Constitutional Power

by Howard Switzer BMRC

In a recent interview with Bret Weinstein about Biden’s abuse of the Presidential Pardon Power by issuing nonspecific general pardons to Fauci and Biden’s own family, Prof. Robert P. George explained that in our Constitutional system when officials fail to protect against such abuses it is the people who are ultimately responsible for its protection and upholding the law. If the people fail to bring swift and certain political retaliation to the people who abuse their powers under the Constitution, we’re just going to get more abuse. I think this is what partially helped Trump get elected.

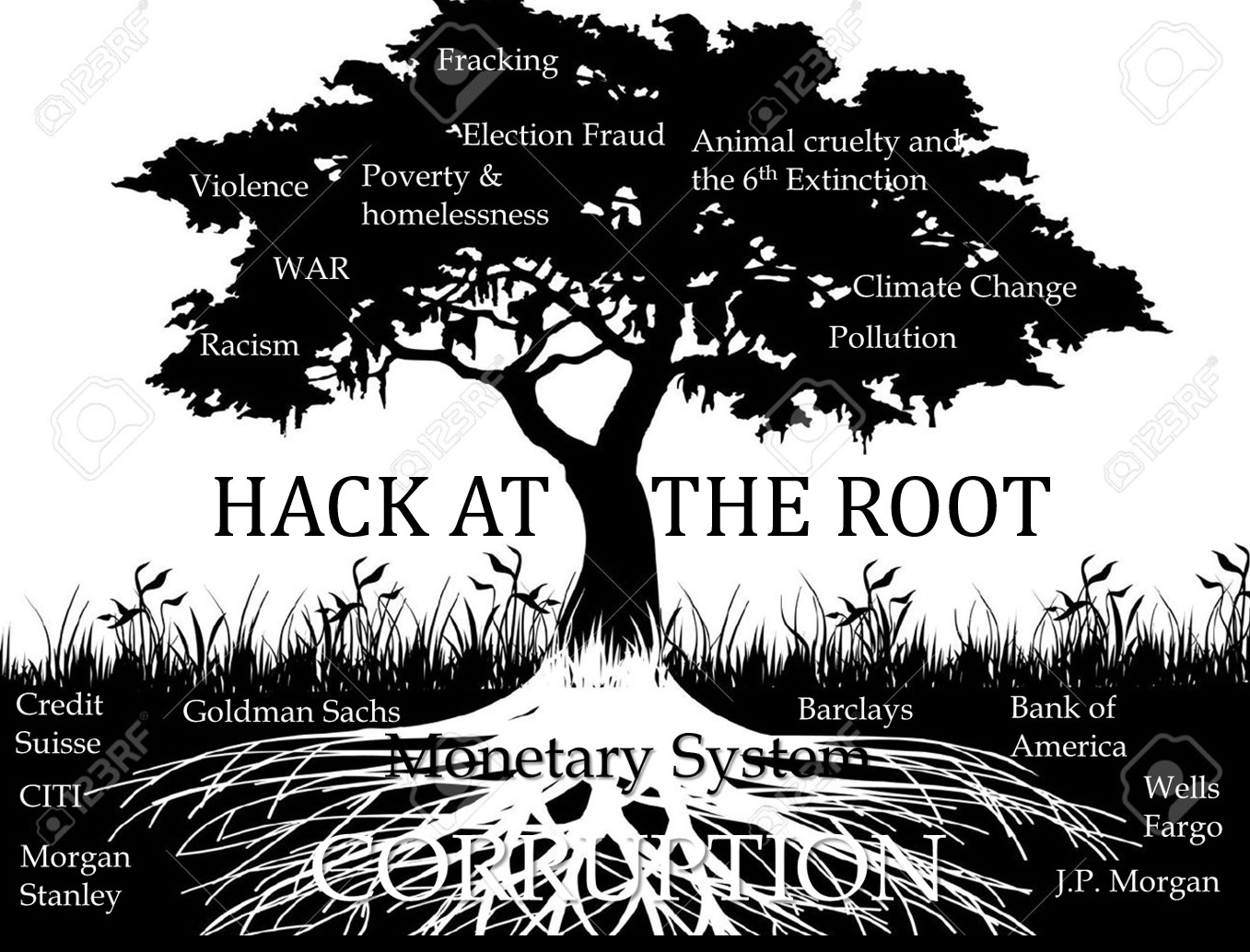

There is a powerful yet heavily censored example of a continuous abuse of Constitutional power, which is Congress's abdication of its Constitutional responsibility to create the nation's money supply for the purpose of fulfilling its Constitutional mandate articulated in the first sentence of the Preamble. This is an abuse of Constitutional power that began over 100 years ago when the nation’s monetary authority was handed over to a private banking cartel. While the people had made it a political issue in the elections around the end of the 19th century, they failed to make the politicians pay the political price. Thus, the abuse continued allowing the banks to crash the economy in 1929, a massive transfer of wealth from the many to the few. While proposals were made to remedy the abuse then they too were rejected, and the abuse continues to this day.

Since there is no political party willing to pursue this abuse of Constitutional power electorally, despite the Green Party having it in their platform, it falls to We the People to raise the issue and make sure both parties pay the political price. Unfortunately, this issue has long been neglected by the academic profession allowing the abusers to escape scrutiny assuring that the public remains ignorant of this abuse and how monetary systems operate. As long as this is the case the public good that is money will remain captured to serve only the interests of the tiny, greedy minority in possession of private wealth.

To allow money to become a source of revenue to private issuers is to create, first, a secret and illicit arm of the government and, last, a rival power strong enough ultimately to overthrow all other forms of government.

– Frederick Soddy

- Our current monetary system is institutionalized usury.

-

- Usury:

- The abuse of monetary authority for personal gain.

- The great religions and philosophers condemned usury.

-

Dante described it as

An extraordinarily efficient form of violence by which one does the most damage with the least amount of effort.