Greening the Dollar

By Howard Switzer GPTN

Putting the Public Back in Public Policy

Eighty-Four years ago, in the face the Great Depression caused by a wide range of abusive practices by the Fed banks, the world's communities of 'Economists' considered the proposal of Dr. Irving Fisher, Dr. Paul Douglas, and several other eminent economists. It was inspired by the work of Frederick Soddy, the father of Ecological Economics, to reform the money system along the lines we now propose. The proposal was supported by some 400 economists, world-around, to restructure our money system from one of private issue and gain to that of public issue and public gain.

This is what Greening the Dollar, the monetary platform of the Green Party proposes. Greens are the only party calling for this reform. Not since the progressive populist era has a political party called for a public money system. Greens should be proud and loud about this because it is the answer to “How are you going to pay for it?” This transformative proposal must become the cornerstone of any effort for ecological and economic balance because the privately controlled profit-motivated monetary system is the primary roadblock to good public policy, foreign and domestic.

In just the 5 years from 2009 to 2014 the 200 most politically active companies in the U.S. spent $5.8 billion influencing our government with lobbying and campaign contributions. Those same companies got $4.4 trillion in taxpayer support — earning a return 758 times their investment. Imagine what those figures look like today! There can be no question as to why public policy does not serve the public interest as that same study concluded that ordinary citizens have zero influence on public policy.

It is rarely reported, but Wall Street banks also own controlling interest in all the major corporations, have representatives on their boards of directors, issue loans to these corporations, and have great influence over the behavior of these corporations. This power and influence is derived from the banks' privilege of creating deposits and issuing loans, for what we all use for money.

Greening the Dollar proposes three simultaneous reforms to change this permanently:

-

Require Congress to be the sole creator of all U.S. money debt-free;

-

End the privilege of commercial banks to create money.

-

Transfer all remaining operations of the Fed to the U.S. Treasury.

The legislation to do this is already written and vetted for 3 years by the office of legislative council. It was introduced in 2011 as the NEED Act. We just need a movement to elect a Congress dedicated to the public interest who will pass these reforms and fulfill, at last, its Constitutional mandate.

This is not a partisan issue; it is the issue of the 99.9%

-

It ends the systematic concentration of wealth to the wealthiest

-

It stabilizes the economy by eliminating the boom/bust cycle, a steady state economy.

-

It sets the economy onto an income basis instead of a debt basis.

-

It would empower Congress to serve the people, making money political again.

Because money controls public policy, money should be a public function not a private privilege.

The BMRC has documentation to support this and can answer any questions a candidate might have.

How Do Banks Profit from Creating Money?

By Rita Jacobs

As we explained in many of our articles published, the banks that make loans create the money for a loan electronically by simply adding digits it to an account. It does not come from any other place. It is NEW money that has been put into circulation in the economy. This is an explanation of how the banks profit from this privilege of creating money.

Let’s suppose that Bank XYZ makes a mortgage loan of $200,000 to John and Jane Doe. For purposes of this illustration, there was no down payment made. They are granted a typical 30-year mortgage loan at 6.0% interest. Below is an amortization schedule of their first three years of monthly payments. Monthly payments remain the same each month throughout the 30 years. The amortization schedule is a record of loan payments that shows the principal amounts and the interest included in each payment. The schedule like the one below generally shows all payments until the end of the loan term. However, we are just looking at the first three years here.

You will note that when the first payment is made that most of the payment goes toward paying interest on the loan. That’s because the interest is calculated at 6% of the 200,000 for a period of one month: $200,000 × .06 ≡ $12,000, which is the annual rate. That is divided by 12 months to arrive at the monthly amount of $1000. Each monthly payment is $11,199.10. After the interest payment of $1,000, the rest of the monthly payment reduces the principal amount of the loan, and the amount owed on the mortgage loan is reduced.

You will notice that the principal amount paid each month goes up slightly, and the interest paid each month goes down slightly. After the first three years of payments, the bank has earned $35,335.76 in interest, while the principal has only gone down by $7,831.84. The interest of $35,335.76 earned by the bank is the bank’s profit on the loan for the first three years. Note that the bank has not invested any of its own money or anyone else’s money in this mortgage. It has simply created it out of thin air.

| Month / Year | Payment | Interest paid | Principal paid | Loan balance |

|---|

| 1 - Jun 2023 | $1,199.10 | $1,000.00 | $199.10 | $199,800.90 |

| 2 - Jul 2023 | $1,199.10 | $999.00 | $200.10 | $199,600.80 |

| 3 - Aug 2023 | $1,199.10 | $998.00 | $201.10 | $199,399.70 |

| 4 - Sep 2023 | $1,199.10 | $997.00 | $202.10 | $199,197.60 |

| 5 - Oct 2023 | $1,199.10 | $995.99 | $203.11 | $198,994.48 |

| 6 - Nov 2023 | $1,199.10 | $994.97 | $204.13 | $198,790.35 |

| 7 - Dec 2023 | $1,199.10 | $993.95 | $205.15 | $198,585.20 |

| 8 - Jan 2024 | $1,199.10 | $992.93 | $206.17 | $198,379.03 |

| 9 - Feb 2024 | $1,199.10 | $991.90 | $207.20 | $198,171.83 |

| 10 - Mar 2024 | $1,199.10 | $990.86 | $208.24 | $197,963.59 |

| 11 - Apr 2024 | $1,199.10 | $989.82 | $209.28 | $197,754.31 |

| 12 - May 2024 | $1,199.10 | $988.77 | $210.33 | $197,543.98 |

| Yearly total | $14,389.20 | $11,933.18 | $2,456.02 | |

| 13 - Jun 2024 | $1,199.10 | $987.72 | $211.38 | $197,332.60 |

| 14 - Jul 2024 | $1,199.10 | $986.66 | $212.44 | $197,120.16 |

| 15 - Aug 2024 | $1,199.10 | $985.60 | $213.50 | $196,906.65 |

| 16 - Sep 2024 | $1,199.10 | $984.53 | $214.57 | $196,692.08 |

| 17 - Oct 2024 | $1,199.10 | $983.46 | $215.64 | $196,476.44 |

| 18 - Nov 2024 | $1,199.10 | $982.38 | $216.72 | $196,259.72 |

| 19 - Dec 2024 | $1,199.10 | $981.30 | $217.80 | $196,041.92 |

| 20 - Jan 2025 | $1,199.10 | $980.21 | $218.89 | $195,823.03 |

| 21 - Feb 2025 | $1,199.10 | $979.12 | $219.98 | $195,603.05 |

| 22 - Mar 2025 | $1,199.10 | $978.02 | $221.08 | $195,381.97 |

| 23 - Apr 2025 | $1,199.10 | $976.91 | $222.19 | $195,159.78 |

| 24 - May 2025 | $1,199.10 | $975.80 | $223.30 | $194,936.47 |

| Yearly total | $14,389.20 | $11,781.69 | $2,607.51 | |

| 25 - Jun 2025 | $1,199.10 | $974.68 | $224.42 | $194,712.05 |

| 26 - Jul 2025 | $1,199.10 | $973.56 | $225.54 | $194,486.51 |

| 27 - Aug 2025 | $1,199.10 | $972.43 | $226.67 | $194,259.84 |

| 28 - Sep 2025 | $1,199.10 | $971.30 | $227.80 | $194,032.04 |

| 29 - Oct 2025 | $1,199.10 | $970.16 | $228.94 | $193,803.10 |

| 30 - Nov 2025 | $1,199.10 | $969.02 | $230.08 | $193,573.02 |

| 31 - Dec 2025 | $1,199.10 | $967.87 | $231.23 | $193,341.79 |

| 32 - Jan 2026 | $1,199.10 | $966.71 | $232.39 | $193,109.40 |

| 33 - Feb 2026 | $1,199.10 | $965.55 | $233.55 | $192,875.85 |

| 34 - Mar 2026 | $1,199.10 | $964.38 | $234.72 | $192,641.12 |

| 35 - Apr 2026 | $1,199.10 | $963.21 | $235.89 | $192,405.23 |

| 36 - May 2026 | $1,199.10 | $962.03 | $237.07 | $192,168.16 |

| Yearly total | $14,389.20 | $11,620.89 | $2,768.31 | |

Let’s presume that after 3 years, that John and Jane Doe decide to sell their house and move. They sell it for $225,000. They need to pay a commission to the real estate broker of 7%. That amounts to $15,750. The government imposes a 2% transfer tax on the sale that amounts to $4,500. The seller must also pay the buyer’s title insurance of $1,200. The cost for the sale is $21,450. These leaves the Does with $203,772. The proceeds are used to pay off the balance of the mortgage, which is $192,168 from your schedule above. This leaves the Does with a profit of $11,604.

When the bank originally made this loan, it added electronic money of $200,000 to an account. The accounting books of the banks show this on the liability side of the bank’s balance sheet. As the principal of this loan is being paid, it reduces the bank’s liability on the balance sheet, and the electronic money is extinguished and removed from circulation in the economy. So the original loan of $200,000 has been loaned, and then extinguished when it is paid off. The bank has not risked any of its own assets or anyone else’s in this transaction. The bank has made a profit of $35,336. Imagine if this had been a loan of $2 billion to a corporation (not at all unusual) payable over 30 years at 5% interest. The bank would have earned interest of $353,360,000.

It is not difficult to see how bankers are able to build up so much wealth and power.

The Savings and Loan institutions (S&L’s) became the primary source of home mortgages in the 1960’s. In the 1980’s the S&L industry fell victim to financial crisis and corruption. Congress removed the walls that separated commercial banks and S&Ls, and the S&L industry today has mostly been folded into the regular banking industry.

Since 1967, residential real estate price inflation has driven home prices to increase by a factor of ten times. In other words, a $100,000 home in 1967 would cost $1,029,290 in 2023. This inflation protects banks in case of a default situation since the inflated house price will likely be more than the loan balance. It also allows banks to collect ever more mortgage interest, and it also greatly increases the opportunity to offer home-equity loans. Because commercial banks create the money used to fund their mortgage loans, the banks are not adversely affected by the price inflation.

STONE COLD REALITY:

U.S. Will Never Repay its $31 Trillion Debt

by Eugene Woloszyn

Republicans, Democrats & media are acting as puppets & clowns as they debate raising the $31 Trillion debt ceiling. This debate has occurred 69 times in the past with no long-range solutions. The Congressional Budget Office (CBO) Long Term Budget Outlook predicts the federal budget deficit will increase from $1,4Trillion per year now to $2.7 Trillion in 10 years. CBO says Gross Federal Debt will increase from $31 Trillion now & go to $52 Trillion in 10 years (1933). This will be an increase of 66% in 10 years. This is obviously reckless & not sustainable. Moreover, US debt estimates have been frequently too low because the US enters unnecessary wars, tax theft by billionaires, & subsidies to Big Business. No one in the mass media, think tanks, schools, politicians, churches will say the obvious: The US will NEVER pay any of these Trillions back, the debts will only skyrocket until the US faces the consequences of all past spendthrift empires: Roman, British, etc.

HOW DOES THE WORLD’S RICHEST COUNTRY GET AWAY WITH THIS?

The US became a debtor nation in the Reagan era in 1985, following Reagan’s huge military increases, while cutting taxes for the 1% & large corporations in 1981 &1986. Stated simply, huge US budget & trade deficits rob the rest of the world. The US forces the World to accept dollars for the $1+Trillion a year in oil, commodities, & cheap consumer goods sent to the US. The key weapon the US uses is the DOLLAR as the reserve currency of the world, which was the product of US victory in WWII. Now, countries are reluctant at holding huge amounts of shaky dollars.

In the early 2000s, countries such as Japan & China accepted these dollars & transformed them into Treasury bonds — both countries holding about $1.4 Trillion each. But both have decreased their Treasury holdings: Japan down by 23%, China down by 34%. Nations don’t trust the US to repay these debts. The third largest holder of US Treasury debt is sidekick Britain with holdings of $646 billion. Cayman Islands holds $283 billion for oligarchs & tax cheats. India & Germany are not even in the top 10. To fill the gap, the FED bought more & more of this Treasury debt & hid it in its bloated balance sheet, which went from $4 trillion in 2019 to $9 Trillion in 2020-2022. This bloated FED balance sheet was coupled to FED encouragement to Wall Street to lend more & thus increase the money supply. The result was sharp INFLATION WORLDWIDE in the second half of 2021.

Admitting it had created a giant error, the FED sharply increased US interest rates. Together with the Ukraine War, this led to wealth around the world fleeing to US for the high interest rates. The value of the dollar soared.

Now economies around the world are suffering Lebanon currency down 98%, Egypt down 50%, Argentine inflation at 100%, Sri Lanka raising electric rates 66% in order to try to get an IMF bank loan. Debts denominated in US dollars are almost impossible to pay with their depressed local currencies. The governments representing 85% of the world population (including India) have not sided with the US or NATO on the Ukraine War. These are warning signs of the US losing its grip on world control.

LIVING PAYCHECK TO PAYCHECK, WHILE THE 1% RAKE IN BONANZA

The 50%-60% of Americans living paycheck to paycheck could’ve grab a piece of the stock & real estate bonanza, triggered by FED a& Wall Street. They also couldn’t afford to buy the sophisticated hedging & tax strategies to protect themselves from the deep stock crash of 2022. This was a product of increases in FED interest rate from one quarter of 1% to 4.5% & rising. To average people, this means credit card interest rates are now near 20%, Amazon, Home Depot 30%. These rates are usurious & not sustainable. In most states prior to the 1960s, populists, unionists & churches pressured state legislatures to enact bans on interest rates over 5%-6%. Bank lobbyists bought state legislators in target states such as South Dakota & Delaware to remove these interest rate caps. The promise was increased financial jobs for credit cards administration. Slowly, all states fell into line. Debtors in the US should consider whether their potential allies should be third world peoples facing similar debt problems or the highflyers on Wall Street or Musk, Bezos & Gates.

Although ordinary people did not benefit from the FED enabled stock & real estate bonanza during the pandemic, we faced the resulting intense INFLATION & INEQUALITY. Business analysts using IRS data reveal that 85% of the wealth gains made possible by FED action during the pandemic in 2020-22 went to the 1%.

WORKING PEOPLE FACE CONSEQUENCES OF FED RECKLESSNESS:

High inflation, uncertainty, & guessing how deep the ensuing recession/crash will be.

A WORKING PEOPLE’S PLATFORM TO COUNTERACT DEBTS

-

Reenact federal & state laws imposing a 6% limit on loans in the US.

-

To show good faith, declare US will repay $1 TRILLION on its federal debt in 2024, after changing appropriate laws.

-

Cut $500 billion from the federal budget from war-making budget items, such as Pentagon, CIA, NSA, nuclear weapon “modernization”, foreign military aid. etc. Also cut subsidies to big business. This might even reach $1 Trillion if courageously done. Do not touch people programs.

-

In a crisis, innovative means must be clawed back from our hidden history. In 1862, President Lincoln faced a funding crisis in the dark hours of the Civil War. Unsure if it would work, Lincoln signed a law creating GREENBACKS, a non-debt currency conceived by US Rep. E.G. Spaulding from Buffalo, NY, who was also a banker. Greenbacks were not borrowed from bankers at interest, but freely circulated based on the productivity of the land & resourcefulness of its people. $450 million were authorized & this amount was never exceeded. It helped to win the Civil War. Bankers hated Greenbacks because they did not get their cut in interest.

GREENBACKS were incorporated into The NEED Act of 2011 introduced by Rep. Dennis Kucinich & John Conyers, but never got out of Committee, because Wall Street feared it. Understanding the mess that Wall Street & its captured FED have created, maybe now the time for GREENBACKS has again arrived.

Why We Need Monetary Reform

By Kevin McCormick, GPTX

In a competition between reform candidates, the candidate who proposes monetary reform will have the strongest argument. The role of money is so essential in our culture and society that one cannot make meaningful reforms without addressing the money question. The question is: "How would you pay for that?"

“Why are these reforms needed?" The answer is that corporations and businesses have no incentive to benefit the public, protect the environment, respect the needs of families, or to contribute to the general welfare. Corporations and businesses are rewarded for mendacious selfishness and penalized for altruism and public service.

We all know the old saying, "Who pays the piper calls the tune." So who, in the United States, pays the piper?

The Federal Reserve banking cartel controls the money system. Commercial banks create deposits to fund loans. These bank deposits are used exactly like money — buying groceries, making payments on debts, child care, buying clothing and other necessities, and saving for a rainy day. The bank loans create over 95% of the money in our economy — the bank financing pays the piper and corporations and social institutions dance to the banking cartel money tune.

It is rarely reported, but Wall Street banks also own the stock of major corporations, have representatives on the boards of directors, issue loans to these corporations, and have great influence over the behavior of these corporations. This power and influence are derived from banks' privilege of creating and issuing loans and deposits.

If the public does not control the creation and issuance of money, then no matter what reforms are made, the financial agenda will ultimately prevail. This is true because the banks and financial interests will be the ones paying the piper. Today, corporate interests are represented by the duopoly parties, Democrat and Republican (campaign finance), by lobbyists, by the corporate media, and so many others whose privileged positions depend on the bank-money Federal Reserve System.

If the public controls the creation and issuance of money, then the public interest will prevail because the public will be the one paying the piper. We need a strong and vital democracy, with broad participation. We need a Congress that serves the public interest, reflects public choices, and responds to public needs and desires — we need a Congress that creates and issues money according to the Constitution: "Congress shall have power ... to coin money and regulate the value thereof . . ."

The public wants a stable and fair monetary system. Congress will be constrained by democracy from excessive inflation or deflation and Congress will have a strong incentive to maintain monetary stability and fairness.

We all know the status quo is deeply unfair with great inequality. We all know that major and even transformational reforms are needed. The foundation cornerstone of reform must be reform of the monetary system by following the Constitution and allowing Congress to exercise its power to coin money and regulate the value thereof. Then the resources and effort for the many reforms we need can be funded and the public interest can be served.

In the universe we can see stars and galaxies and we can derive constellations and many measurements. But the unseen and virtually undetectable dark matter causes the universe to behave as it does. In our society we can see injustice, inequality, consumerism, environmental destruction, political divides, etc. What we do not perceive is the cause of society’s characteristics and shape. The monetary system is the “dark matter” that causes society to behave as it does.

Let us pay the piper and let us call the tune.

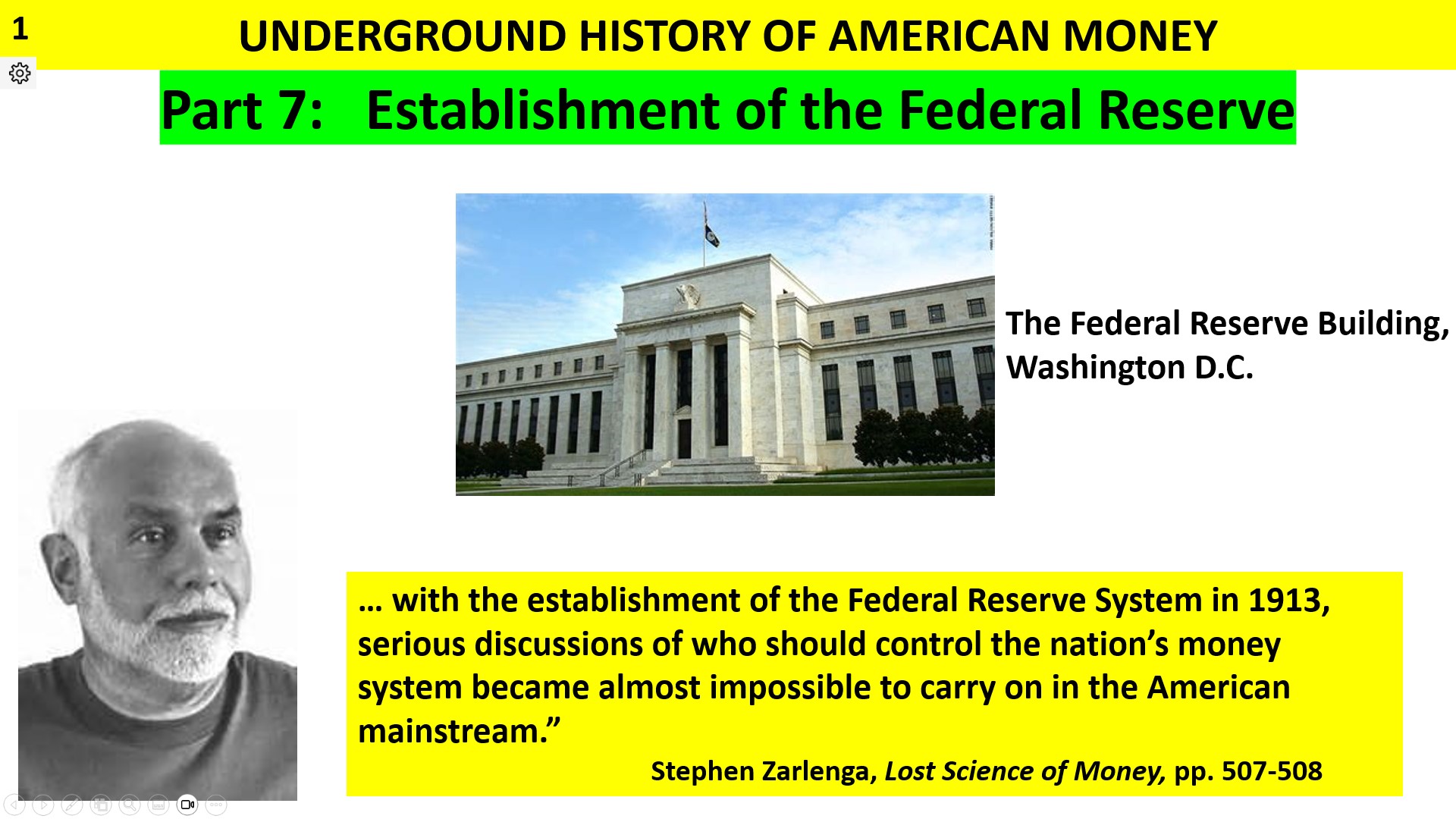

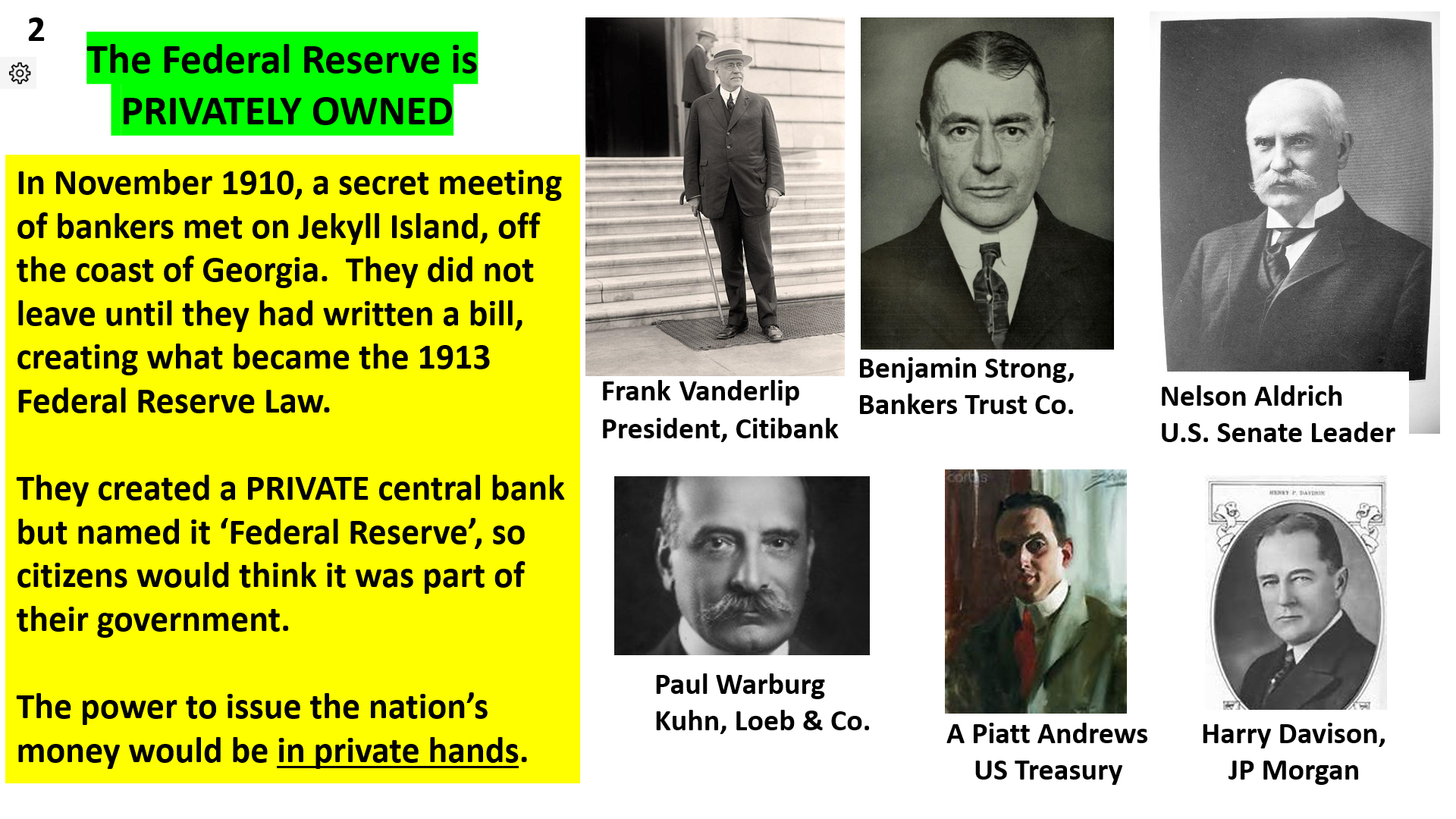

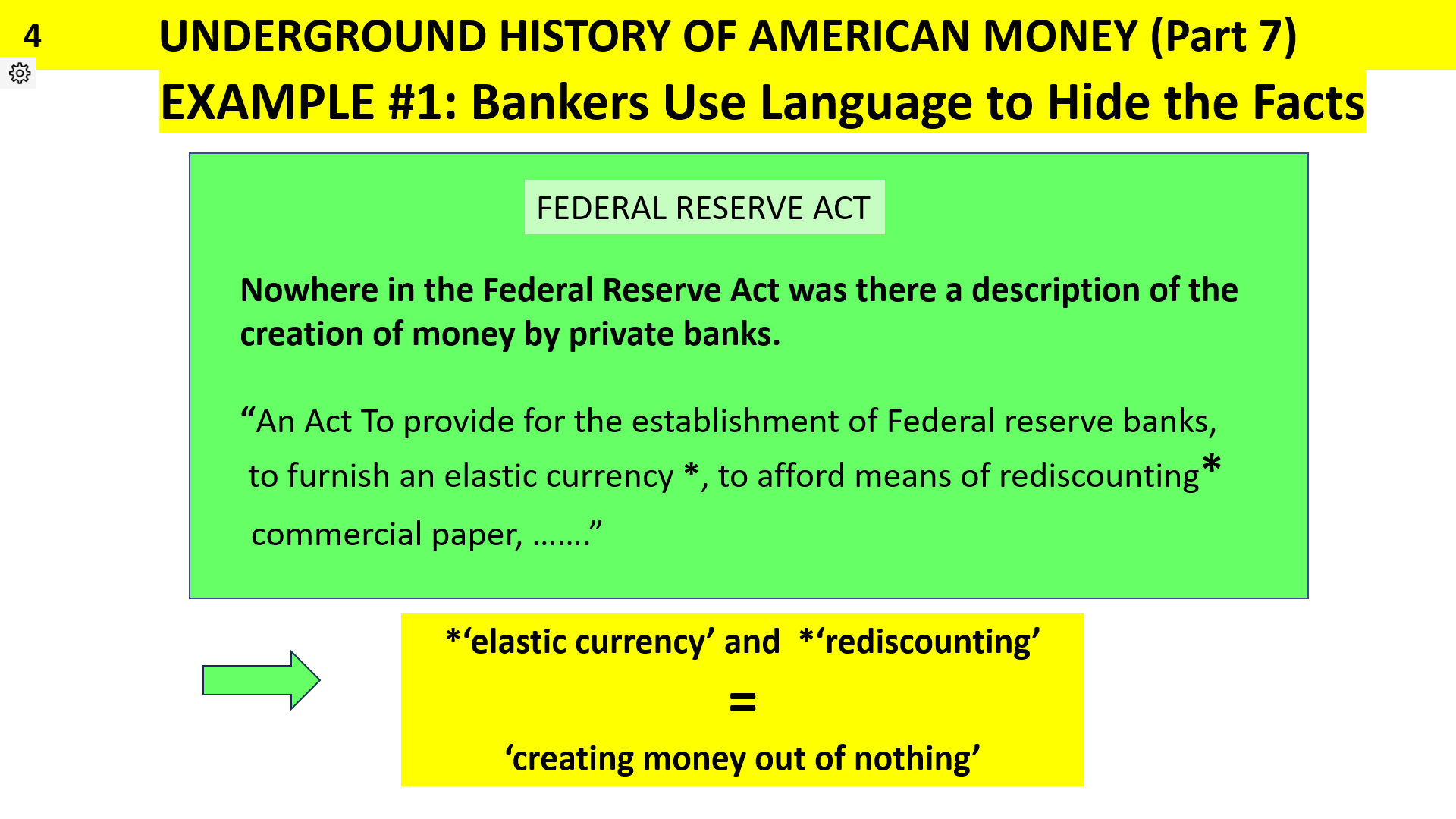

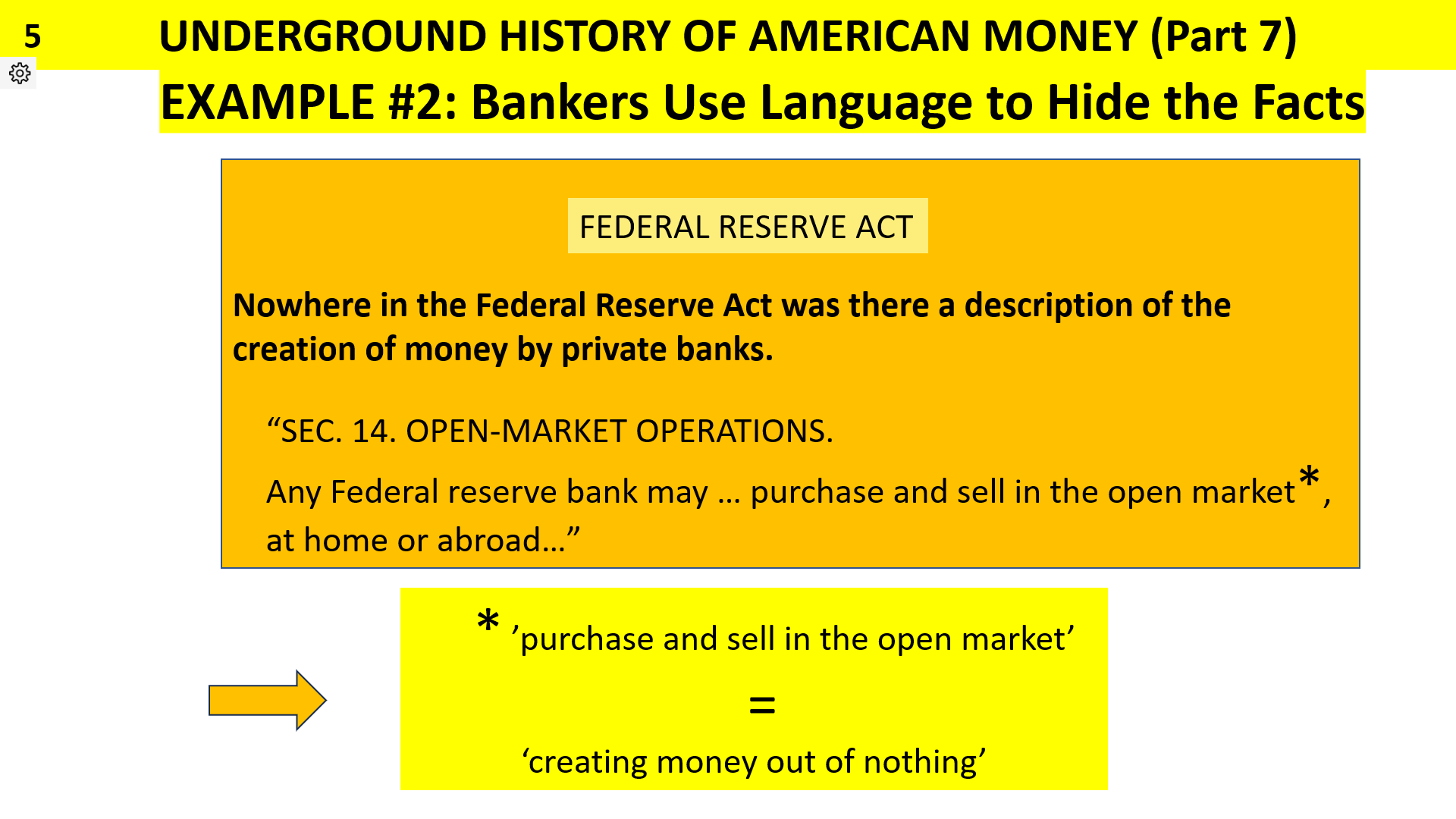

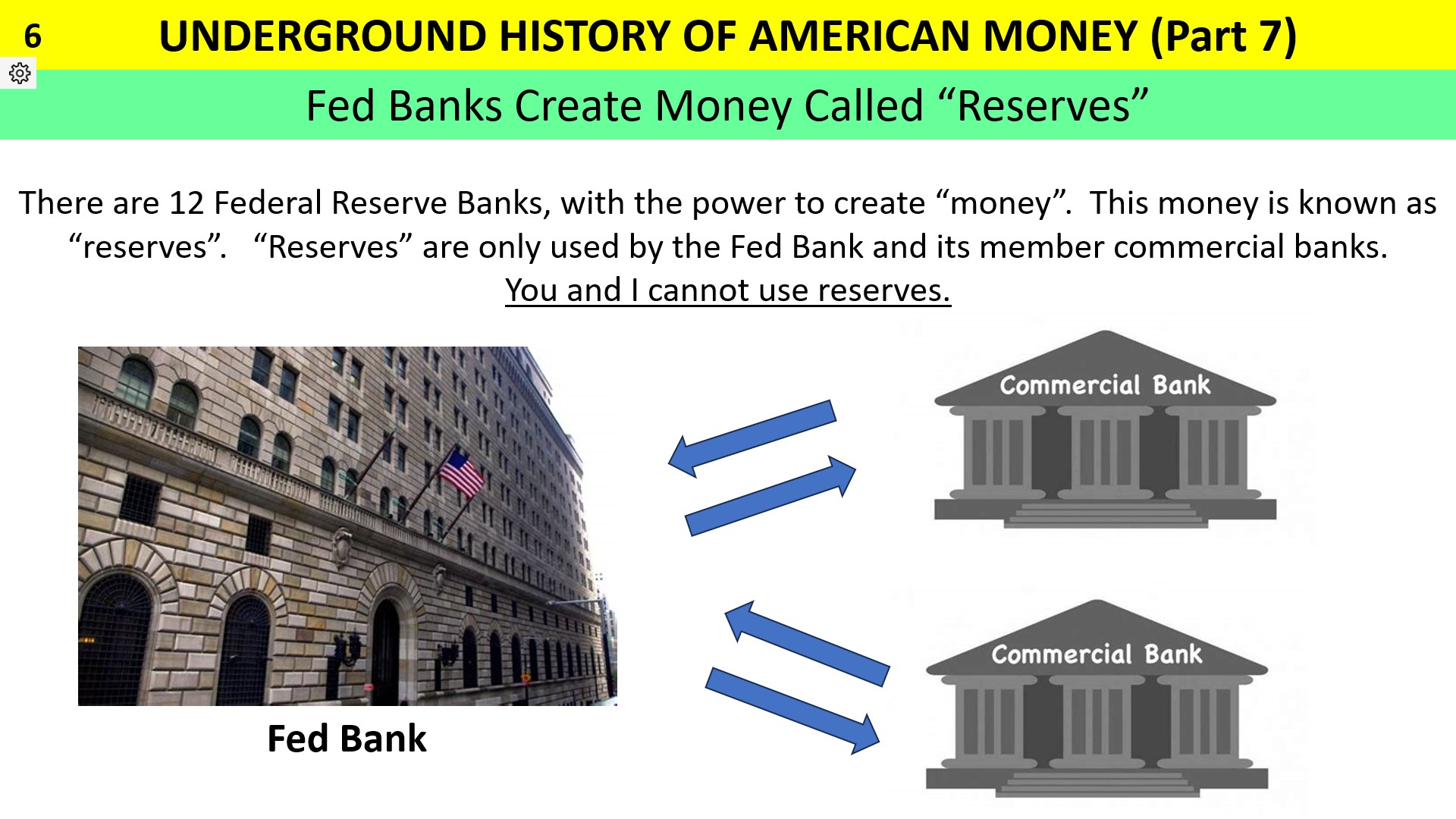

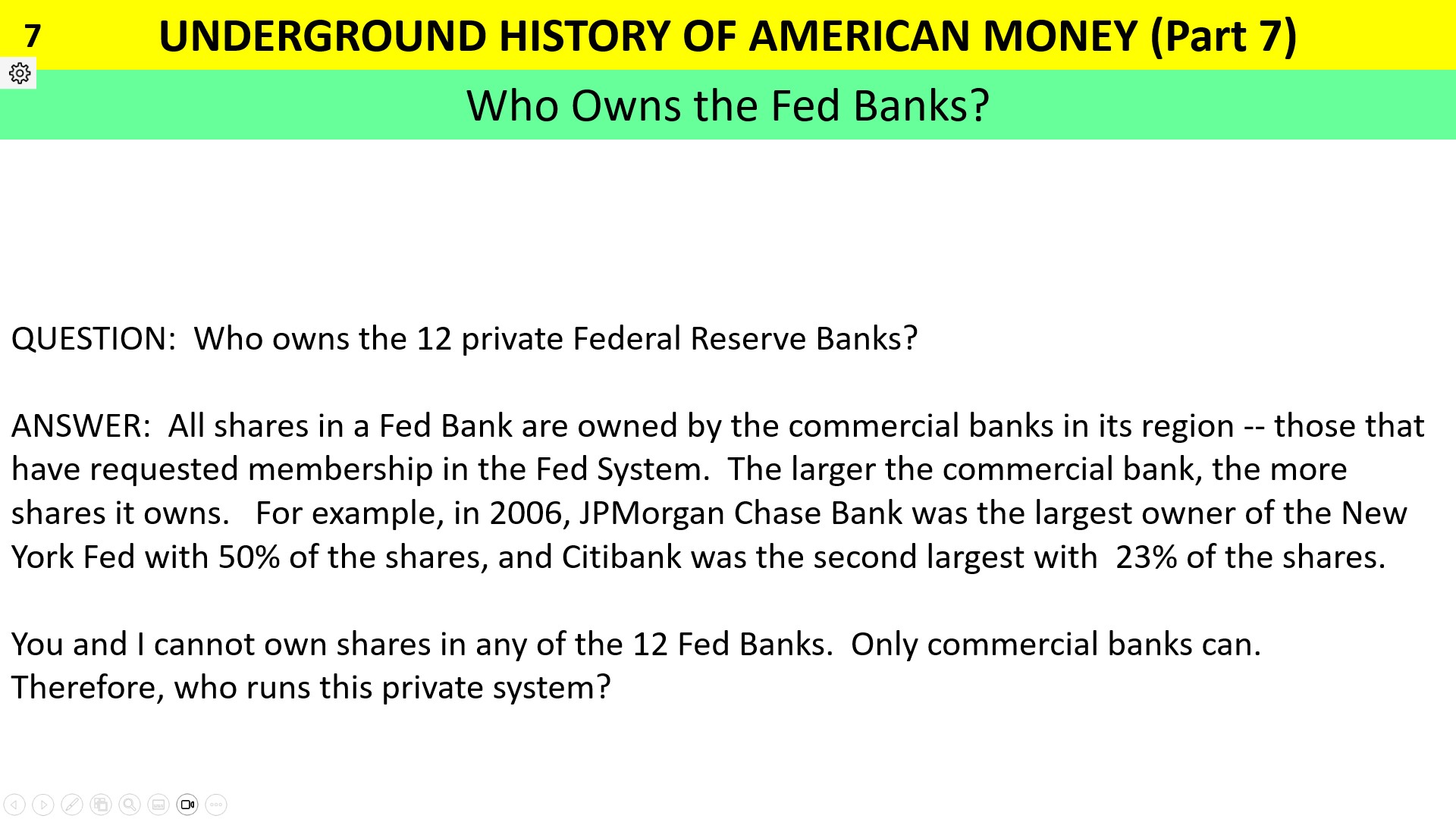

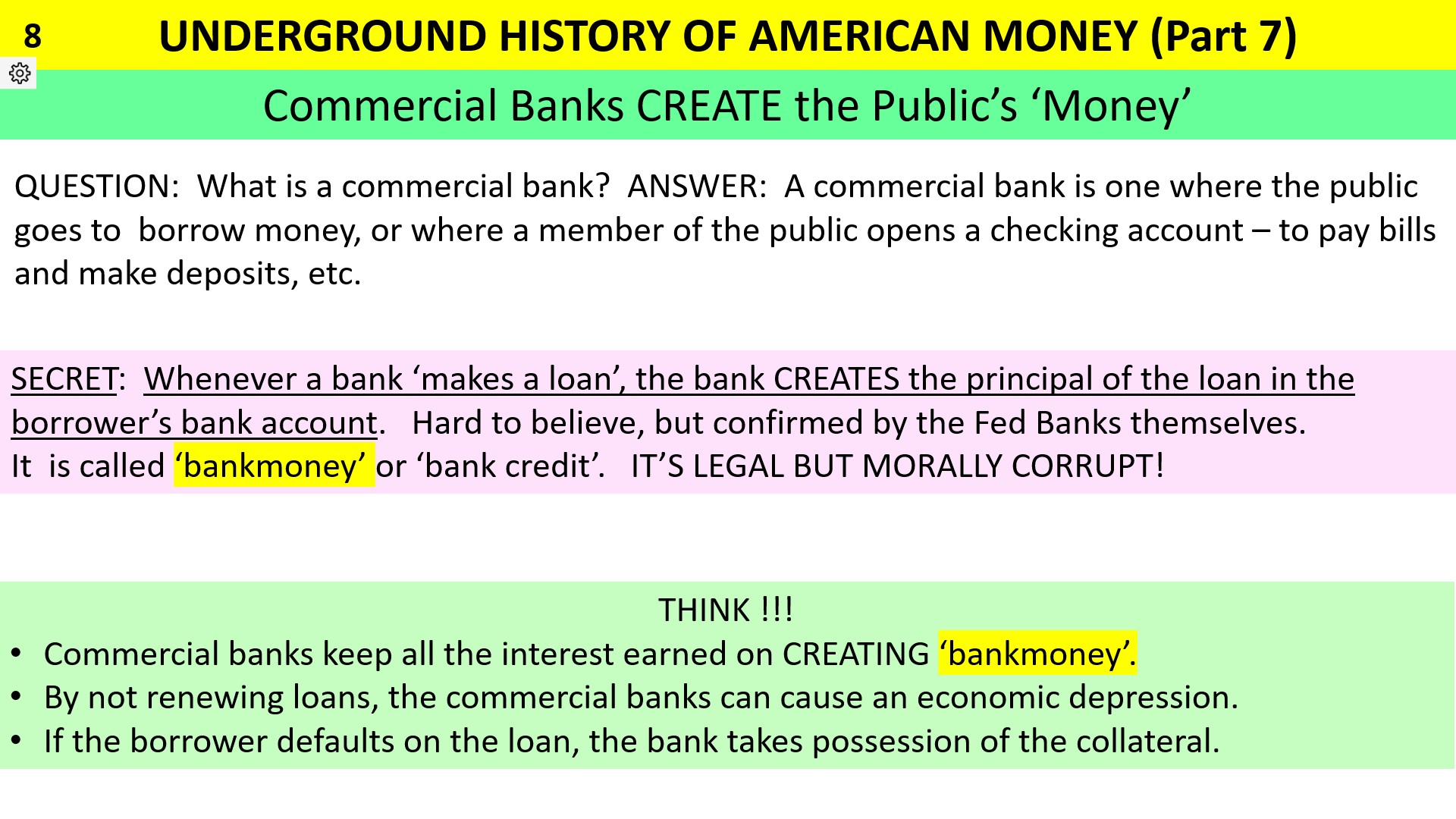

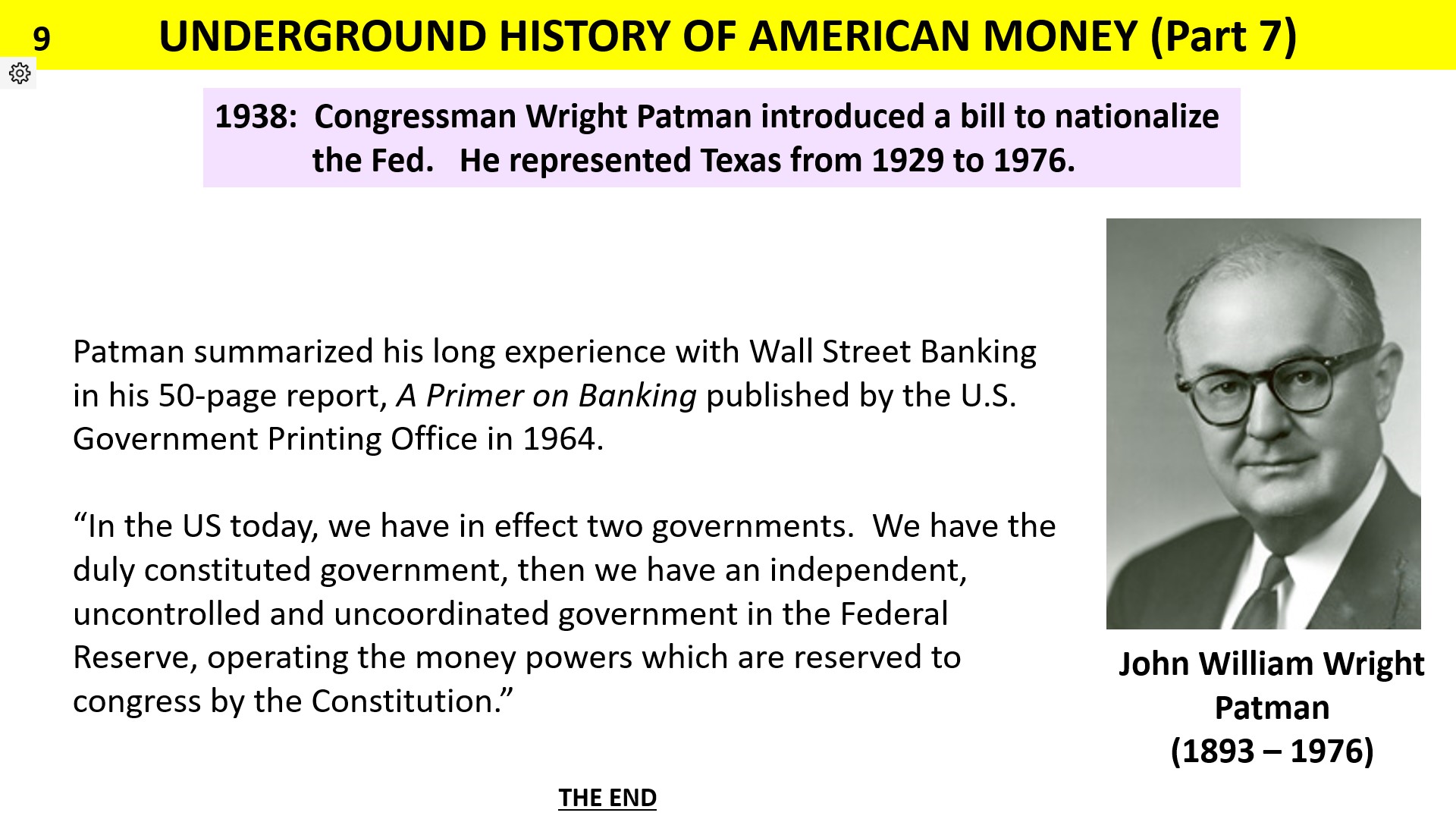

Underground History of Money — Part 7

By Sue Peters GPNY

The Most Important History is the History We Don't Know — Alexander del Mar

By Howard Switzer

Alexander del Mar (aka Alexander Del Mar and Alexander Delmar; August 9, 1836 – July 1, 1926) was an American political economist, historian, numismatist and author. He was the first Director of the Bureau of Statistics at the U.S. Treasury Department from 1866 to 1869.

Del Mar was a rigorous historian who made important contributions to the history of money. During the mid-1890s, he was distinctly hostile to a central monetary role for gold as commodity money, championing the cause of silver and its re-monetization as a prerogative of the state.

He believed strongly in the legal function of money. Del Mar dedicated much of his free time to original research in the great libraries and coin collections of Europe on the history of monetary systems and finance. He wrote:

"In the United States the same bag of coins often masquerades now as the reserve of one bank, and now of another. How far similar subterfuges are employed in the various private banking establishments of Germany is not known, and in the absence of such knowledge it is deemed safer to include the entire paper issues in the circulation. This at least is a known quantity; the 'reserves,' as experience has too often and too sadly proved, may only exist in the playful imagination of that fortunate class who have secured the prerogative to issue bank money."

- Our current monetary system is institutionalized usury.

-

- Usury:

- The abuse of monetary authority for personal gain.

- The great religions and philosophers condemned usury.

-

Dante described it as

An extraordinarily efficient form of violence by which one does the most damage with the least amount of effort.