There are many writers today analyzing our dire ecologic and economic circumstances that comprise an existential threat to civilization and perhaps even to life on this planet. Numerous aspects of the problem have been and continue to be discussed with few solutions presented as the capitalist economic system continues its assault on all life for profit. Even though to plant a field, drill an oil well or manufacture a widget requires money, just as any political or military campaign does, money is seldom discussed and is generally misunderstood.

The nascent monetary reform movement understands that the real cause of the extreme wealth inequality as well as the destruction of our resource base, is the monetary system. It is a systemic problem that affects human behavior as well as our planet. The movement understands, as did Aristotle, that money for most of civilization's history has played two roles:

An exchange medium for facilitating economic activity (it is just money)

An instrument of power capable to dominating the market (the hidden hand)

So, the question is, how can we change the system to retain the first role and eliminate the latter? To do this we must understand the monetary system we have. There are three characteristics of the current monetary system that bestow power on the undeserving.

It systematically concentrates wealth to the wealthiest (plus compounding interest)

It is capable of being hoarded (withheld from the economy for speculation)

It has superior liquidity to goods and services

Hoarding large amounts of money gives one the power to disrupt the economy for their own benefit, as Charles Koch, Bloomberg, Bill Gates and other politically active billionaires have done. This power to disrupt also enables hoarders of money to demand the payment of interest as a tribute to their allowing some money to circulate. Any discussion of changing the monetary system requires a discussion of governance — asking who rules? Such a change will require a political intervention to change the rules that allow the undeserving elite to rule. Setting aside the political intervention required for the moment, let us look at which rules need to be changed.

First, we need to recognize that our monetary system is privately controlled by the big banks and their largest capital holders. All our money is created by the commercial banks when individuals, businesses, or governments borrow money. The loan amount is created simply by entering the amount into the bank’s electronic ledger plus interest. This electronic money, or checking account money, comprises about 97% of the money supply, the rest is in cash printed by the government but sold to the banks for cost of production. The government also mints coins, the smallest category of the money supply, and they are sold for face value for which the government gets seigniorage (the face value minus the production costs). The production cost of the coins is of course more than the production cost of the paper bills which is about 2 cents per bill regardless of its denomination.

The banking system does not lend existing money held on deposit as the folk-knowledge myth would have us believe. Instead, keystrokes create credit as new money in your bank account, all of which you are required to pay back with interest in a set amount of time. The money, representing the principle of the loan is created this way but the money representing the interest, also part of the debt to be repaid, is not. Since this is how all our money is created system wide the money to pay the interest must come from the principle of another loan. This creates predatory competition and a constant imperative for economic growth, all of which is geared for making profits. While the de-growth movement discusses the problems of economic growth it does not seem to be aware of the growth imperative built in into the monetary system. Thus, any effort by government to provide healthcare, transportation, housing, etc. is opposed by those representing the donors and owners of the profit-seeking private money system.

Further complicating matters, the money created by the loan is extinguished, eliminated as the principle of the loan is paid off leaving less money circulating in the competition to pay the interest. The interest money is not destroyed as it is the banks profit after paying its expenses. For the system to function more loans must continuously be made to pay the interest and keep ahead of the money being extinguished. When loan payments (money destroyed) exceed loans being made (money created) we have a recession or depression because there is not enough money circulating in the system, and this happens reliably every 10 to 12 years. As you can see the system incentivizes a hyper competitiveness to pay debt and leaves a lot of losers in its wake, not the least of which is the ecosystem that all life depends on and from which all wealth is extracted.

Our nation’s Constitution articulated the purpose of the government established by We the People in the very first sentence, “ to form a more perfect Union, establish Justice, ensure domestic Tranquility, provide for the common defense, promote the general Welfare, and secure the Blessings of Liberty to ourselves and our Posterity” The Constitution also provides the tools necessary to accomplished this, but Congress has consistently ignored its responsibility, having turned over monetary authority to its privately owned central bank established in 1913 which is controlled by its large member banks. The Federal Reserve Act was justified and passed to stabilize the banking system and economy but was creating problems in less than 10 years and in 1929 caused the Great Depression. The Pecora Commission investigation proved this, but again, while legislation was passed, it was inadequate to the task and did not change the monetary system to provide long-term economic stability. The world’s top economists proposed the solution in 1933 with the Chicago Plan which later became the 1939 Proposal for Monetary Reform but the forces of private Money Power had captured the allegiance of the majority in Congress and it was not passed. Like the Greenbacks, it was proposed that government issue the money and to protect the system the private banks were to be banned from creating deposits, returning monetary authority to elected government.

Congressman Dennis Kucinich, after years of trying to get good legislation passed, came to the realization that none of the needed legislation for healthcare, education, infrastructure and an effective response to climate change would ever pass until Congress took back the monetary authority to issue the money to fund it. In 2011, as a response to the 2008 crash and with the help of the American Monetary Institute (AMI), he wrote and introduced the National Emergency Employment Defense Act (The NEED Act) which contained the same three changes proposed in 1939. The very next year the private money funded political system gerrymandered him out of his seat.

AMI is a monetary thinktank that holds an international conference for monetary reform every year in Chicago and was instrumental in forming the International Movement for Monetary Reform (IMMR). In 2017 several AMI members decided the movement needed a more active American organization to educate about money and The Alliance for Just Money was born, Their mission is to educate the electorate about the money system and promote the idea of changing it. The three essential reforms are:

Return the nation’s monetary authority to government.

Ban the private creation of money by the commercial banks.

All money is created by government and issued for the general welfare.

These three reforms will empower elected government to do all the things for which they are elected by the people. However, there is still that one function of money they do not address and that is the trillions in privately hoarded money that can be used to buy government influence and dominate the economy. To address that issue, government can simply apply a demurrage fee — which is a parking fee for money — that discourages hoarding and increases the circulation velocity, allowing government to do more with less. This will drive the hoarded money being used against people and planet back into circulation.

However, as we have seen and experienced, a political intervention at the national level is nearly impossible due to the private money-controlled mass media and political system in place. Political intervention at the state level too may be difficult as well with the Koch Network funding campaigns and legislation through ALEC, an organization that gives corporate interests outsized influence. That leaves us with our local governance, county, town, or municipality. As communities did during the Great Depression, local governments can issue currency to allow the full utilization of local labor and material resources. The Federal Government (AKA the big banks who own the FED) will try to repress this activity and citizens must be prepared to resist efforts to keep them from their rightful prosperity.

The events of 1932-1933 in Wörgl, Austria demonstrated the power of a currency with a steadily declining value that is restored with a weekly demurrage fee. The local government issued only $6000 worth of the currency and accomplished $2.5 million in public projects in just 15 months. It was so successful hundreds of towns world-around wanted to duplicate it. Irving Fisher, one of the authors of the 1939 bill, even wrote a 1933 booklet titled Stamp Scrip which explained how to do it, saying it could end the depression in weeks. Unfortunately, the powerful central banks had governments ban the scrip and Wörgl went back to 30% unemployment and depression.

We the People may not be desperate enough to change the monetary system yet but the longer we wait the worse our circumstances will be. People should understand the monetary alternatives to the status quo currently crushing all life in this world. With that knowledge we may be able to avoid total catastrophe.

LOCAL CURRENCIES CAN HELP REVIVE JOB CREATION & FAMILY INCOMES

By Eugene Woloszyn, GPCT

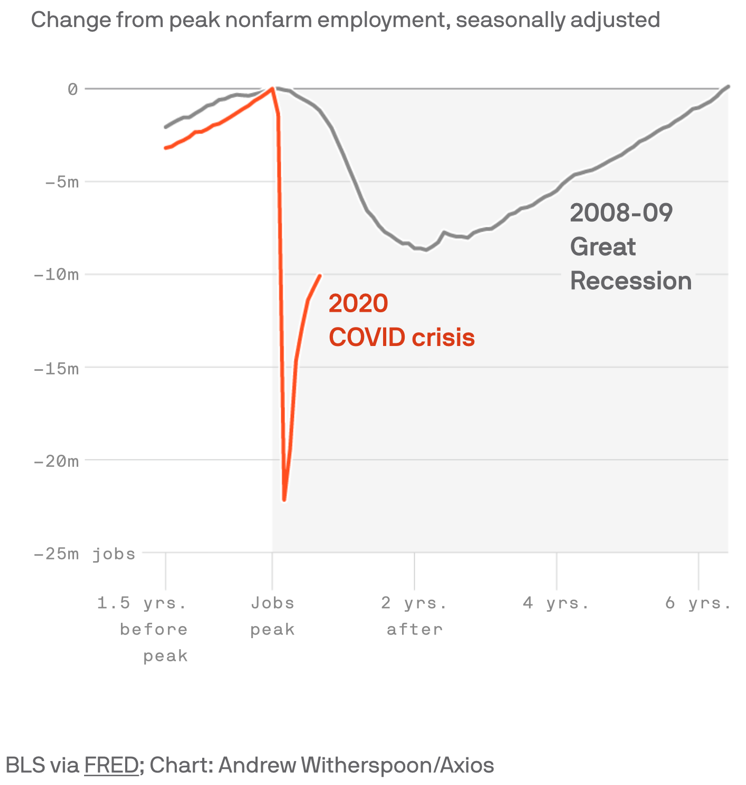

There are 10 million fewer jobs now than Feb 2020. Crisis in health coverage, rents, mortgages, & insufficient food. Generous Federal aid to corporations, but little new aid to working people since CARES ACT in 3-2020 — 10 months ago.

Realistically, future government aid to working families will probably be too small and too late.

After the election, Wall Street and Stock Markets were gleeful with a Democrat controlled House and a Republican controlled Senate. This meant further stalemate on laws to help working families and no reversal of the $1.5 Trillion in tax cuts for the 1% and corporations enacted in 2017.

SIT BACK PASSIVELY OR ORGANIZE LOCALLY?

Should we sit back passively & hope for the best or dig back in the past for historical examples of how working families self organized to defend their standard of living?

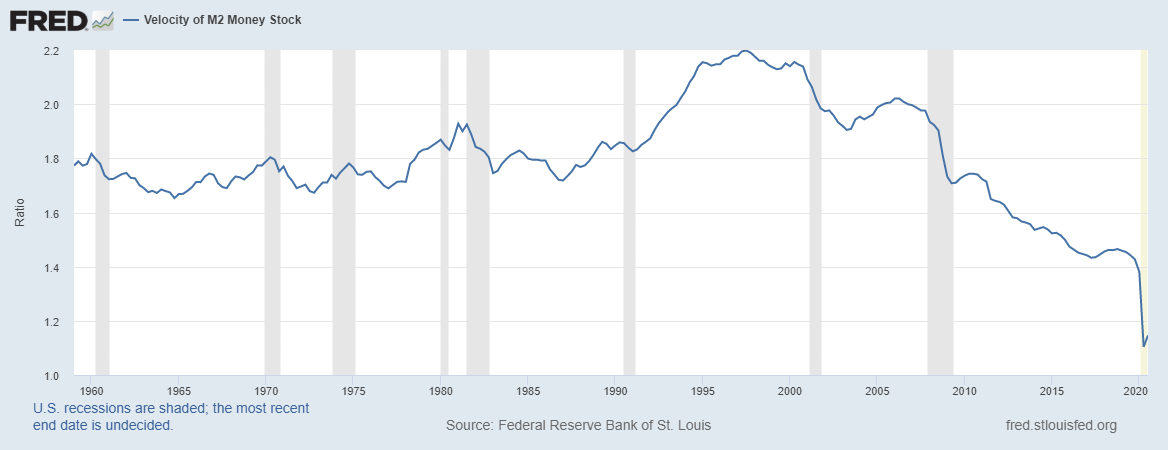

The VELOCITY of Money describes the number of times dollars circulate in an economy over a standard period of time. “High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions.” Investopedia, 11-29-20.

US money velocity peaked at 2.2 in 1997 and has fallen continuously by 50% to about 1.06 or lower in late 2020 — an all time recorded low. This is a gigantic fall and means money is acting sluggish and retarding job growth and street level commerce. This did not start with Covid, but is 23 years old and a very steep decline.

WHY DON’T WE HEAR ABOUT THIS DANGER AND A PLAN TO REVERSE IT? WHY SILENCE FROM THE MASS MEDIA & GOVERNMENT LEADERS OF BOTH MAJOR PARTIES?

Several factors are involved, but common sense makes clear that US money is not allowed to circulate in local communities. Rather, each night chain store businesses and banks whisk away gross profits and cost of new inventory to headquarters and money center banks in NYC. The very next day, this hot money may be in creating jobs in Brazil or India, in commodity speculation, or in secret bank accounts in low tax havens on tiny islands around the world. Our chain store purchases don’t create jobs in our towns, but in super-profitable sites around the world.

IS THERE A WAY TO INCREASE MONEY CIRCULATION?

As we have reported previously, Lincoln in 1862 faced an existential threat even worse than Covid. The North was losing militarily and had run out of money, with big NYC banks demanding outrageous interest rates. After much worry and fear, Lincoln approved an unorthodox plan. $450 million in no-debt Greenback dollars were created, based on the present capabilities of the Northern population, its industrial base, and the future inventiveness of its people. This money paid soldier salaries and war equipment and won the war. Similarly, Congress and the President could do the same now and bail the US out of this crash. Trillions in Greenbacks could put people back to work on infrastructure repair, electric micro-grids, (reasonably priced) nationwide wi-fi, and a transition to an enhanced Medicare for All and a Green New Deal. These are popular measures, with polls showing majority citizen support. But both major parties are controlled by Wall Street and keep this off the table.

CAN A LOCAL CURRENCY HELP TO INCREASE MONEY CIRCULATION?

Local currencies were used in the 1930s Depression with surprising success in Switzerland and in the small town of Wörgl, Austria. After 3 years of Depression in Wörgl, the town was devastated, broke, and industry collapsed. A local currency was suggested by the Mayor, approved by the town council, and officially started on July 31,1932. It was enthusiastically accepted and used for 13 months, stimulated local construction, town improvements, and many new hires. In June 1933, Worgl’s mayor held a briefing on the plan in the capital, Vienna. 170 Mayors present felt the plan should be implemented in their towns. Fearing expansion of the public money currencies, the Austrian Central Bank and Austrian courts shut down the experiment on September 1, 1933. It was so successful it was known as The Miracle of Wörgl. See more at The Miracle of Wörgl

Local currencies have been tried in a few places in the US since the 1980s. But, they were usually created by a volunteer group in a college town and most eventually petered out. From the experiences of the 1930s and more recently in the US, a number of features can make local public currencies successful. Here they are:

Money is a governmental responsibility and must be approved by the town council and accepted for paying local taxes.

It will require an intensive educational campaign. Only a few towns would have the courage to take this on against expected local and regional opposition. But the level of desperation in 2021 and feelings of abandonment by the federal government will be a big factor in deciding local submissiveness or anger and action.

Big Banks, their publicists, lobbyists, and advertising dollars can be expected to oppose the plan as it would challenge their control of the money system. However, a success in one town could open the floodgates (like the 170 Mayors in Austria who wanted to copy the Wörgl plan).

If passed by a town, the town should authorize the currency, establish the rules, and create a network for its functioning such as businesses accepting the currency. Heavy emphasis should be placed on food purchase using the public currency and assisting area farms to increase production. A major goal is creation of a reasonably priced, healthy food distribution network in the town.

A citizen public information campaign would seem to be necessary, coordinated with sympathetic council members. This should be explained as an emergency measure in a crisis situation that requires creative, new approaches.

Trading Economic Growth for Economic Justice and Sustainability

By Howard Switzer, GPTN

Jason Hickel wrote an excellent article for the guardian four years ago titled To Deal With climate Change We Need a New Financial System which explained how our debt-based money system drives climate impacting growth. This is Jason Hickel’s response to new book by Robert Pollin and Noam Chomsky called, Climate Crisis and the Green New Deal written because he objected to the framing they used regarding “degrowth.” In the book they made the assertion:

“The fact of the matter is, degrowth is not a solution, just in terms of simple mathematics. Let’s say we cut global GDP by 10 percent, which would be a bigger depression than the 1930s. What happens? We cut emissions by 10 percent. It’s no solution at all.”

As Jason notes, they missed the point, “… more growth requires more energy use, and more energy use makes it impossible for us to cover it with renewable alternatives,” the primary mechanism being promoted to reduce emissions. However, he says, “… the notion that to reduce emissions to zero we have to reduce economic activity to zero is obviously ridiculous.” I agree.

Clearly economic activity has been conflated with economic growth just as capitalism has been conflated with free-enterprise and while I know that Jason understands this, he fails to mention the mechanism that systematically drives economic growth. That mechanism is the money. All our money is created and issued exclusively by the private for-profit banking system as interest bearing debt. In this system the principal of the loan is created as a deposit in one’s account but not the money required to pay the interest. That money must come from another’s loan principal and drives growth as society competes to pay the interest on their loans to avoid a default and losing all their real wealth collateral.

By ending the private bank-money system and implementing instead a public money system we can create “… a different kind of economy altogether: one that is organized around the interests of human well-being and ecology, rather than around the interests of capital.”

The institutions that create and distribute money in our nation and throughout much of the world are diseased.

Monetary systems are supposed to ensure that economies are healthy, just and sustainable. They shouldn't benefit the 1% at the expense of the rest of us.

The COVID-19 pandemic has exposed and worsened the inherent crises in our medical and economic system. The same is true of our monetary system, which in its own right is as invisible, harmful and widespread as the virus, but was unjust, unsustainable and undemocratic long before the first cough, sneeze, or breath from a coronavirus-infected person occurred on US shores.

The Federal Reserve System, our nation's central bank, composed of 12 Regional Reserve Banks, creates money out of thin air -- as do all commercial banks across the country.

The Fed will be issuing money in the current crises by literally entering numbers in bank accounts of some corporations as loans and to other corporations to purchase assets, mainly corporate bonds. The Fed will create the money and decide the major corporate recipients of the trillions. It will also dole out an additional several hundred billion dollars from the government's recent stimulus bill to large corporations.

A return to economic "normalcy" post COVID-19 won't happen and shouldn't be our goal. Now is the time to organize for economic and political systemic change, including a democratized money system that will serve the interests of people and communities over those of Wall Street and other financial interests.

* * * *

The U.S. Constitution (Art 1, Sec 8) authorizes Congress to "coin" (a verb) money. Money creation, along with spending and taxes, are the three major economic tools of the federal government. Federal spending and tax policies (which receives the most public attention) repeatedly favor the super rich and corporations - including the several trillion dollars worth of bills recently passed by Congress. Monetary policies are different. They not only favor the rich and corporations. The corporations are the decision-makers.

Without a shot being fired or tanks rolling into the nation's capital, corporate interests pulled off a financial corporate coup with passage of the 1913 Federal Reserve Act — capping a century long struggle between banksters and the public over who (or what) should have the right to have their hand on our nation's money spigot.

Our current monetary system is institutionalized usury.

Usury:

The abuse of monetary authority for personal gain.

The great religions and philosophers condemned usury.

Dante described it as "An extraordinarily efficient form of violence by which one does the most damage with the least amount of effort."

THE MOST IMPORTANT HISTORY IS THE HISTORY YOU DON’T KNOW:

By Howard Switzer, GPTN

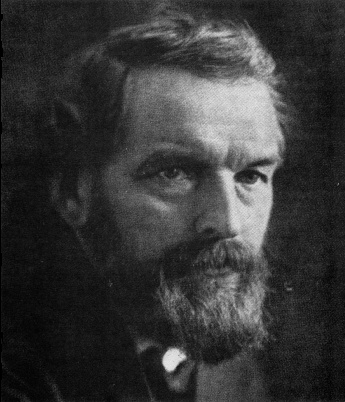

Silvio Gesell

Silvio Gesell was a merchant entrepreneur and monetary theorist. His ideas were implemented in a small town, Wörgl Austria, in 1932, in the depth of the Great Depression which went from 30% unemployment to 100% employment. This publicly issued money was the most successful currency in history. His book, The Natural Economic Order contained his proposal for Free Money and Free Land, similar to the land rent proposal of Henry George. His central point was that money should be a pure exchange medium.

“Only money that goes out of date like a newspaper, rots like potatoes, rusts like iron, evaporates like ether, is capable of standing the test as an instrument for the exchange of potatoes, newspapers, iron and ether. For such money is not preferred to goods either by the purchaser or the seller. We then part with our goods for money only because we need the money as a means of exchange, not because we expect an advantage from possession of the money.”

“So we must make money worse as a commodity if we wish to make it better as a medium of exchange.”